Genetic Discrimination & Health Insurance: An Analysis

Shivam Goel

24 March 2018 2:59 PM IST

According to Order VIII, Rule 6 (3), Illustration (c) of the Code of Civil Procedure, 1908, ‘insure’ means to secure payment of a sum of money in the event of loss or damage to property, or, death or physical injury to a person in consideration of the payment of a premium and observance of certain conditions. ‘Insurance’ is a contract by which a person (insurer) in consideration of a sum of money (the premium), becomes bound to secure a party against the risk of loss occasioning from certain events marked out by the contract. The party deriving security from the contract is called the ‘insured’ and the contract itself is termed as ‘Policy of Insurance’.

‘Policy of Insurance’ is a document containing an undertaking in consideration of premium, to pay a specified amount or part thereof in the event of a specified contingency. According to Section 2(9) (c) of the Insurance Act, 1938, risks covered by an insurance, or, the protection afforded by an insurance is called an ‘insurance cover’.

A contract of insurance like other contracts is concluded by offer and acceptance and if there is a stipulation that the liability will attach itself under the contract only if premium is paid, then, that will be a condition precedent to the policy taking effect.

As per Section 2(d) of the Insurance Act, 1938, the word ‘insurer’ includes: (a) persons actually carrying on insurance business; (b) persons about to commence insurance business; and (c) persons who have stopped insurance business but against whom claims or liabilities might be outstanding.[1] According to Section 65 (58) of the Finance Act, 1994, ‘insurer’ means any person carrying on the general insurance business or life insurance business in India. Tersely, an ‘insurer’ is the person who assures against the loss[2] and according to Section 2 (8) of the Companies Act, 1913, ‘insurance company’ means a company that carries on the business of insurance either solely or in common with any other business or businesses.[3]

According to Section 49 of the Transfer of Property Act, 1882, ‘insured’ is that in respect of which insurance has been obtained, and, the person indemnified by his contract of insurance is called a ‘policy holder’. Lastly, ‘insurable interest’ is a financial or legal interest which an insured must have in the person, object or activity covered by an insurance policy.

‘Health’ is a state of complete physical, mental and social well being[4] and not merely an absence of sickness, disease or infirmity.[5] ‘Health’ is not merely ‘soundness of body’[6] but is rather freedom from sickness and/or suffering of all kinds (physical, mental and social). Health is a state of being hale, sound or whole in body, mind, soul and well being.[7] ‘Health Cover’ or ‘Health Insurance’ means the effecting of contracts which provide sickness benefits or medical, surgical or hospital expense benefits, whether in-patient or out-patient, on an indemnity, reimbursement, service, prepaid, hospital or other plans basis, including assured benefits and long term care.[8] ‘Good health’ as employed in insurance contract, ordinarily means a reasonably good state of health[9]; it means that the applicant has no grave, important or serious disease, and is free from any ailment that seriously affects the general soundness and healthfulness of the system.[10] Good health does not mean a condition of perfect health.[11] To be ‘healthy’ means to be free from disease or bodily ailment, or any state of the system peculiarly susceptible or liable to disease or bodily ailment.[12] ‘Illness’ in the context of insurance law signifies a disease or ailment of such a character as to affect the general soundness and healthfulness of the system seriously, and not a mere temporary indisposition which does not tend to undermine (weaken) the constitution of the insured.[13] It is important to note that in the context of life insurance, ‘serious illness’ means an illness that permanently or materially impairs, or is likely to permanently or materially impair, the health of the applicant. Not every illness is serious; an illness may be alarming at the time, or thought to be serious by the one afflicted, and yet not be serious in the sense of that term as used in insurance contracts. An illness that is temporary in its duration, and entirely passes away, and is not attended, nor likely to be attended, by a permanent or material impairment of the health or constitution, is not a serious illness. It is not sufficient that the illness was thought serious at the time it occurred, or that it might have resulted in permanently impairing the health.[14] Similarly, ‘infirmity’ in the context of insurance law signifies an ailment or disease of a substantial character, which apparently in some material degree impairs the physical condition and health of the applicant and increases the chance of his death or sickness and which if known would have been likely to deter the insurance company from issuing policy.[15]

Genes are responsible for the various traits that human beings possess, and it is the difference in these traits that make one homosapien different from the other. While the genes pass on several positive traits (characteristics), but they could at times be responsible for some abnormal medical conditions which are passed on from one generation to another; these abnormal medical conditions which are passed on from one generation to another are called genetic disorders. Genetic disorders can be dominant or recessive. If the gene is ‘dominant’ then the disease will surface, but if the gene is ‘recessive’ then the trait will not show up but because the individual is the carrier of the gene, he/she can pass it to the next generation.

According to the National Human Genome Research Institute[16], there are broadly three types of genetic disorders: (a) Monogenetic disorders[17]; (b) Multi-factorial inheritance disorders[18]; and, (c) Chromosome disorders[19]. There are plethora of medical conditions which can partially be attributable to genetics and partially to the lifestyle and dietary habits of an individual. Therefore, comprehensive ‘genetic testing’ is required in order to determine whether a particular medical condition is an outcome of a possible genetic disorder, or, whether a particular medical condition is a result of the environmental conditions, lifestyle and dietary habits of an individual.

Exclusion of Genetic Disorders from Insurance Claims:

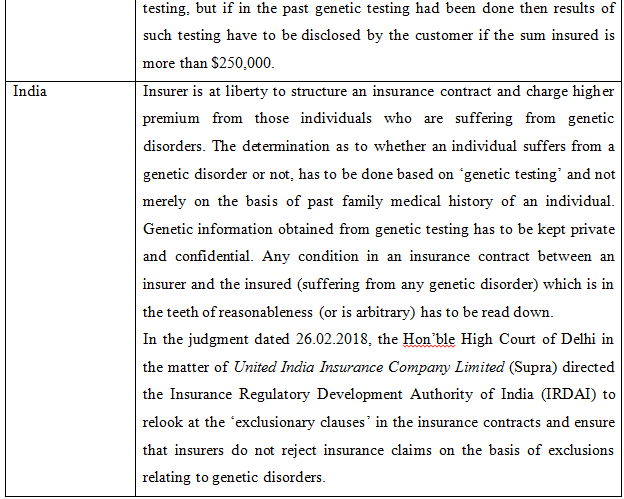

Right to healthcare is an integral part of the right to life guaranteed under Article 21 of the Constitution of India, 1950. Healthcare without health insurance, with the medical costs escalating each year, is a serious challenge. Health insurance cover with the exclusion of ‘genetic disorders’ batters the most basic right of an individual to avail insurance for the prevention, diagnosis, management and cure of diseases. Actions (policy decisions) of the insurers in excluding any particular category of individuals, that is, those with genetic disorders, from obtaining health insurance are not only per se discriminatory in view of Article 14 of the Constitution of India, 1950, but are also violative of a citizen’s right to health enshrined in Article 21 of the Constitution of India, 1950. Covenants, stipulations and/or clauses of an insurance policy must stand the test of reasonableness as ‘insurance’ is a means of social security.

The Hon’ble High Court of Delhi in its report dated: 26.02.2018 in the matter of, M/s. United India Insurance Company Limited v. Jai Prakash Tayal[20] has held that:

- If genetic heritage of a particular individual puts him in a risk of developing a particular disease (e.g. cancer) then this cannot to be used against him by the insurer to deny him from availing an appropriate health insurance cover.

- In order to exclude ‘genetic disorders’ from insurance claims, there has to be genetic testing, and the data collected from such testing needs to be preserved and confidentiality has to be maintained. Without carrying out genetic testing and prescribing what is the kind of genetic disorder which is excluded, applying a ‘general exclusion’ albeit genetic disorders in insurance covers leads to arbitrariness.

- Exclusions in insurance contracts such as the ones relating to genetic disorders do not remain merely in the realm of contracts but overflow into the realm of public law, thus, reasonableness of such clauses is subject to judicial review. The broad exclusion of genetic disorders is thus not merely a contractual issue between the insurer and the insured but spills into the broader canvas of ‘right to health’. The broad exclusion of genetic disorders from insurance contracts (or claims) is illegal and unconstitutional.

- If insurance policy is issued to an individual without carrying out genetic testing then his/her insurance claim cannot be declined merely on the basis of ‘exclusion of genetic disorder’ stipulated in the insurance cover based on the family medical history of the insured, in absence of specific test been conducted by the insurer at the time of issuance of the insurance cover to the insured.

- Pure genetic disorders (such as: Huntington’s disease and Down syndrome) can be treated differently by the insurer in the insurance policies, however, exclusion of the entire gamut of disorders which are hypothetically genetic would be totally illegal and arbitrary.

- As far as health insurance is concerned, exclusion of genetic disorders in all forms would be contrary to public policy. There are several prevalent medical conditions which affect a large mass of population such as: cardiac conditions, high blood pressure and diabetes in all forms, all these medical conditions can be classified as genetic disorders, however, the entire purpose of taking medical insurance would be defeated if all these genetic disorders are excluded from the applicability of an insurance cover.

- Insurers are at liberty to structure their contracts (health insurance covers) based on empirical testing and data. Blanket exclusion of ‘genetic disorders’ from health insurance covers in bad in law. A ‘genetic disorder’ needs to be determined by the insurer by conducting ‘genetic testing’, and not merely by analysing the family medical history of the insured.

- Insurance contract is a ‘standard form of contract’ and usually the insured is made to sign the dotted line. It is unrealistic to assume that an insured reads each and every clause of an insurance contract before signing it. On most occasions, an individual who intends to obtain insurance has no choice to say ‘no’ to a clause in the insurance contract. Medical insurance is primarily obtained for the purpose of unforeseen medical conditions which may affect a person and so long as there has been no fraud, concealment or suppression at the time of obtaining insurance, policies ought to be honoured.

- An individual suffering from genetic disorder needs medical insurance as much as other individuals. Insurers are at liberty to structure insurance contracts in a way that no prejudice is caused to the interest of the insurance company on one hand, and, on the other hand an individual suffering from a genetic disorder is not put to any serious peril. Insurance companies are at liberty to prepare specialised contracts (medical insurance covers) for individuals suffering from genetic disorders bearing in mind that all terms of the insurance policy must survive the test of reasonableness and non-arbitrariness.

- Pure genetic disorder (such as: Huntington’s disease and Down’s syndrome) can be treated differently in insurance covers, however, blanket exclusion of entire gamut of disorders which are speculatively genetic would be contrary to law.

Renewal of Insurance Policy: A renewal of insurance policy means repetition of the original policy. When an insurance policy is renewed, the policy is extended and the renewed policy in the identical terms from a different date of its expiration comes into force.[21] Any change in the terms and conditions of an insurance policy which are significantly different from the original policy stipulations must be specifically consented to by the insured at the time of renewal of the policy, and, the insurer is not allowed to slip in new terms and conditions at the time of renewal of the policy without bring them specifically to the knowledge and attention of the insured.

Takeaways:

- Insurance companies cannot deny health insurance to individuals suffering from genetic disorders.

- Insurance companies are to determine whether or not an individual suffers from genetic disorder, based on genetic testing and not on the basis of past family medical history of an individual.

- Insurance companies are under a legal duty to protect and safeguard the information received by them qua an individual derived from genetic testing; high degree of confidentiality is to be maintained.

- Insurance companies can charge higher premiums from individuals suffering from genetic disorders based on the doctrine of intelligible differentia but have to comply with the tests of reasonableness and non-arbitrariness. Article 14 and Article 21 of the Constitution of India are required to be complied with in letter and in spirit.

- Blanket exclusion of genetic disorders from health covers is not purely a contractual issue between the insurance company and the insured but rather the same spills into the canvas of right to health. Primacy is to be given to a contract, but no contract can override the fundamental rights enshrined in the Constitution of India, 1950.

- That vide notification dated 19.03.2018 (Ref: IRDAI/HLT/REG/CIR/046/03/2018), IRDAI taking note of the directions issued to it by the Hon’ble High Court of Delhi in the matter of M/s. United India Insurance Co. Ltd. v. Jai Prakash Tayal (RFA No. 610/2016 & CM Nos. 45832/2017) has instructed all the insurance companies offering contracts of health insurance to not to include ‘genetic disorders’ as one of the exclusions in the health insurance policies issued in respect of all their existing health insurance products and also in the new products launched and/or filed under the provisions of Guidelines on Product Filing in Health Insurance Business (Ref. No. IRDA/HLT/REG/CIR/150/07/2016) dated 29.07.2016.

[1] V.F. & G. Insurance Co. v. Fraser and Ross, AIR 1960 SC 971, 976

[2] Section 2(6), The Life Insurance Corporation Act, 1956

[3] An ‘insurance company’ is an institution which undertakes to pay a sum of money on the death of the assured, or at any other fixed time, in consideration of premiums, assessments, or payments made in any other way.

[4] Kirloskar Brothers Ltd. v. Employees’ State Insurance Corporation, AIR 1996 SC 3261

[5] CESC Ltd. v. Subhash Chandra Bose, AIR 1992 SC 573

[6] Section 144 (1), The Criminal Procedure Code, 1973; Article 25 (1) of the Constitution of India, 1950

[7] Venable v. Gulf Taxi Line, 105 W. Va. 156, 141 S.E. 622, 624

[8] Regulation 2(f), The Insurance Regulatory and Development Authority (Registration of Indian Insurance Companies) Regulations, 2000

[9] Kroon v. Travelers’ Insurance Co., 290 Ill. App. 35, 7 N.E. 2d 935, 937

[10] Mincy v. Washington National Insurance Co., 130 Pa. Super.285, 196 A. 893, 897

[11] White v. Sovereign Camp, W. O. W., 184 S.C. 215, 192 S.E. 161, 165

[12] Bell v. Jeffreys, 35 N.C. 356

[13] Prudential Insurance Co. of America v. Sellers, 54 Ind. App. 326, 102 N.E. 894, 897

[14] Fishbeck v. New York Life Insurance Company, 179 Wis. 369, 192 N.W. 170, 175; American National Insurance Company v. Hicks, Tex. Civ. App., 198 S.W. 616, 622

[15] Eastern Dist. Piece Dye Works v. Travelers’ Insurance Co., 234 N.Y. 441, 138 N.E. 401, 404, 26 ALR 1505

[16] National Human Genome Research Institute, https://www.genome.gov/19016930/faq-about-genetic-disorders/, Last viewed: 17.03.2018

[17] These are caused by mutation in a single gene, e.g. sickle cell disease.

[18] These are caused by a combination of genetic and environmental factors, e.g. diabetes, cardiac diseases, and cancer (some forms).

[19] These are caused due to either deficiencies or excesses of the genes or due to structural changes in the chromosomes, e.g. Down’s syndrome and chronic myeloid leukaemia.

[20] RFA 610/2016 & CM Nos. 45832/2017, High Court of Delhi, Prathiba M. Singh, J.

[21] Biman Krishna Bose v. United India Insurance Co. Ltd. & Anr, 2001 (6) SCC 477